Simply put, we don't buy overvalued stocks...EVER.

The time to rotate to value stocks is here. Valuation and strong fundamentals MATTER. This time is not different from previous market cycles.

We know this is hard to hear for traditional growth investors because during the past ten to fifteen years simply buying the dips in the S&P 500 produced higher returns. Now faced with rising interest rates, and an increasing likeliness the economy falls into a recession, investors need to return to a prudent style of investing and avoid the temptation of the FATMAAN (Facebook, Alphabet, Tesla, Microsoft, Amazon, Apple and NVIDIA) companies.

These companies now comprise more than 25% of the S&P 500 and approximately 50% of the NASDAQ. With years of access to historically cheap debt, the FATMAAN has bloated to record weights (and their indexes to record highs along with it). As their access to this cheap debt begins to extinguish, so too will their growth, and consequently their returns. In short, in this rapidly changing economic environment, we expect the FATMANN that all growth investors have become familiar with, to start looking much leaner in the years to come.

This time is similar to the collapse of technology stocks during the 2000 bubble. However, this time is even worse as not only are valuations working against these companies, but also the Federal Reserve will not be able to bail out the tech sector with low interest rates since it is forced to fight higher inflation.

As such, rather than investing in growth/momentum, investors should be seeking quality companies selling below their intrinsic value as these companies will perform better in a rising interest rate environment while also offering better protection during a recession.

Given the historic outperformance of growth vs value stocks leading up to a potential recession, we are not surprised the tides are finally turning (see chart below).

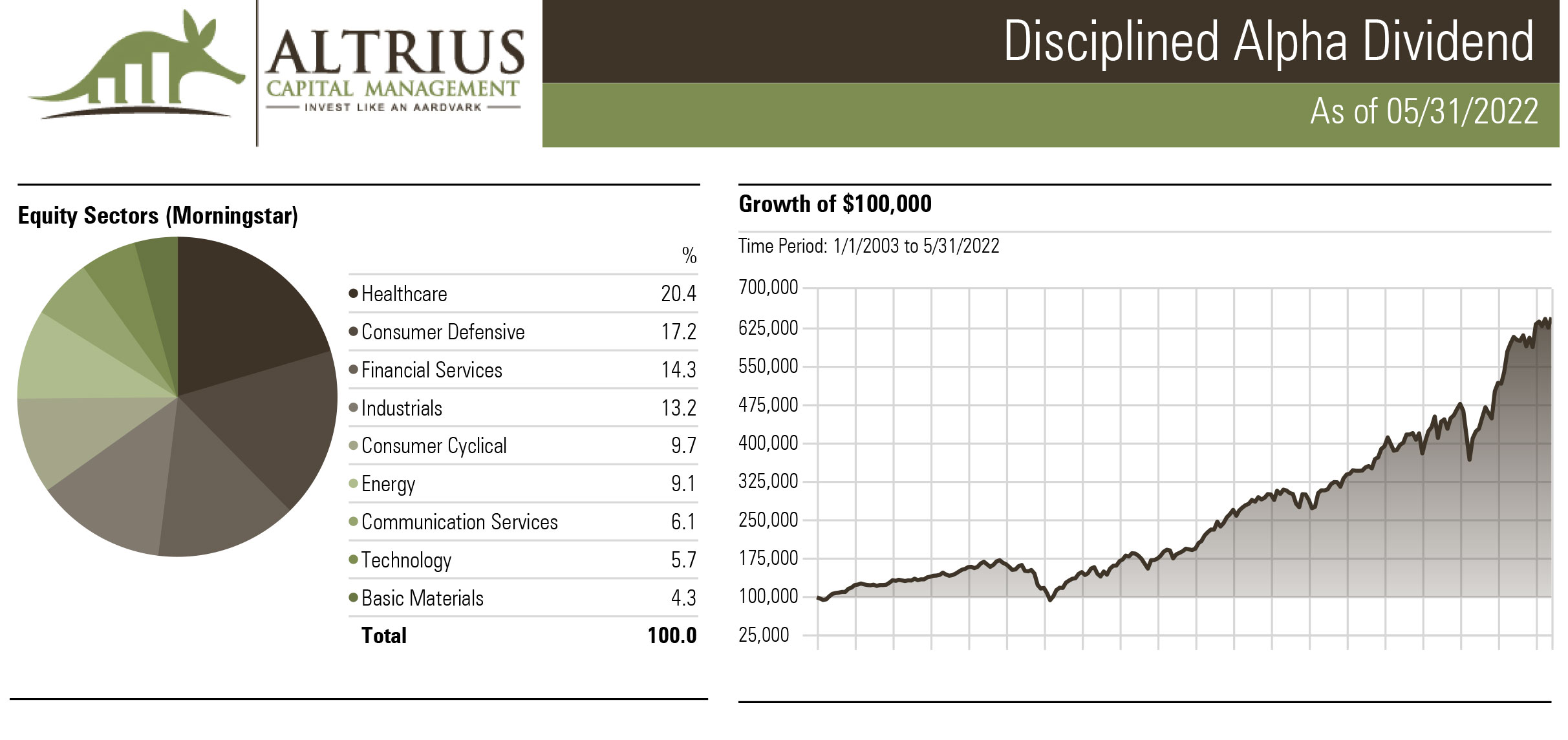

Our performance is a testament to our disciplined, time-tested strategy, which since our inception in 2003 has returned 10.07% annually and have garnered “Manager of the Decade” honors from PSN Informa in 2020 while significantly outperforming our index over the last 3, 5, 10 and 15 years. (*Disciplined Alpha Dividend)

Our investment thesis is simple, invest in companies at reasonable valuations that pay dividends. We get paid to wait for modest capital appreciation. It might be boring, but it helps us achieve our objective to “participate in rising markets, perform in sideways markets, and protect while providing income in declining markets.”

Altrius Disciplined Alpha vs IWD - SPY.pdf

As always, should you have any questions about our investment process or your personal financial circumstances, please don't hesitate to contact us.